Benefits on the Clock

Medicaid and SNAP are getting harder to keep while HSAs just got easier to use. Here's the plain-language, no-panic breakdown of the 2026 changes, plus the deadlines that matter for your family.

Here's a sentence nobody wants to read on a Tuesday: the benefits a lot of our families count on are getting harder to keep, and the paperwork to prove you still qualify is landing in mailboxes right now.

If that makes your stomach drop a little, take a breath. This isn't a doom post. It's the opposite. Because at the exact same time some doors are getting narrower, a genuinely useful one is opening wider, and most people have no idea it happened. Two clocks are running. This is your heads-up on both, in plain language, with the dates that actually matter.

A quick, honest note before we start: I'm not a financial advisor or a lawyer, and nothing here is personalized advice. This is a Builder's field guide to what changed, so you can ask the right questions and make your own call. Rules also vary by state, so your local Medicaid or SNAP office is always the final word.

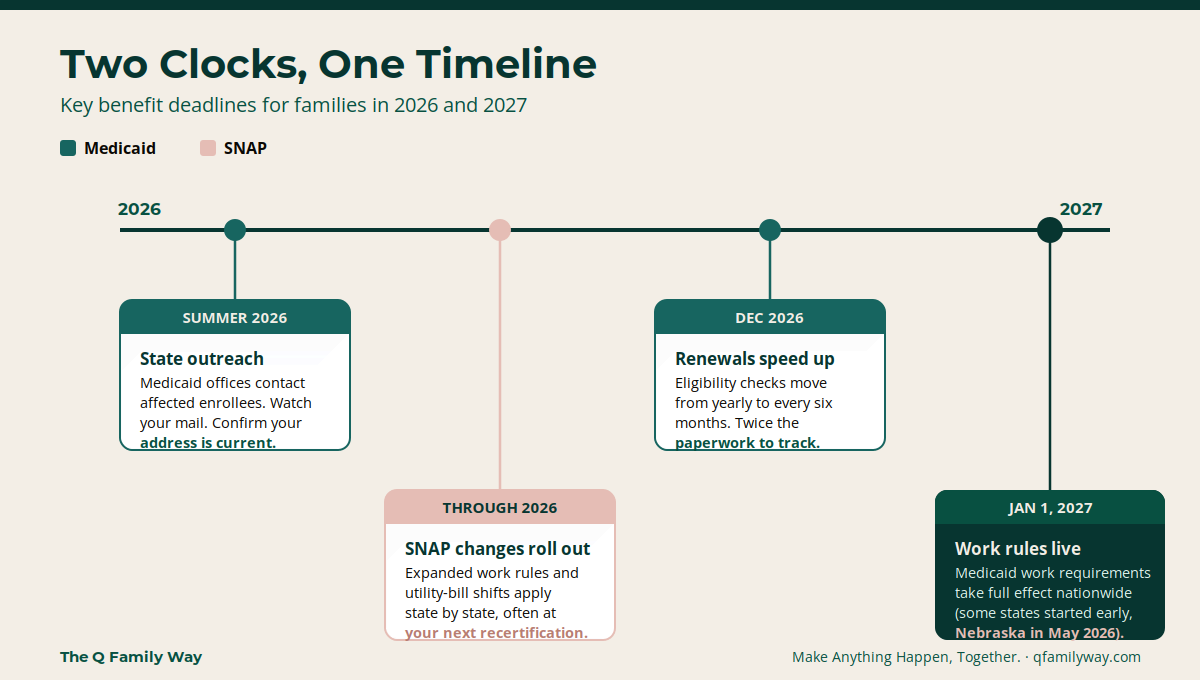

Clock One: Benefits Are Getting Harder to Keep

In July 2025, a large federal budget law (you may have heard it called the One Big Beautiful Bill Act) reshaped how Medicaid and SNAP work. The headline is the same for both programs: work requirements, tighter check-ins, and more paperwork to prove you still qualify.

Most people affected are already working or already qualify for an exemption. The real risk for our families isn't that you don't meet the rules. It's losing coverage in the shuffle - like a letter you didn't see, a deadline you didn't know about, or a form that didn't get submitted in time. That's the part you can actually get ahead of.

Medicaid: what changed

- The 80-hour rule. Non-exempt adults ages 19 to 64 in the Medicaid expansion group will need to complete at least 80 hours a month of work, volunteering, school, or job training to keep coverage.

- More frequent renewals. Eligibility checks move from once a year to every six months, which means twice the chances to get tripped up by a missed letter.

- The timeline. States must have the requirements running by January 1, 2027, though some are starting sooner (Nebraska went first, in May 2026). States are required to do outreach to affected enrollees between roughly late June and the end of August 2026. If you're on Medicaid, watch your mail this summer.

- Who's exempt. Pregnant and postpartum people, caregivers of a child under 14, full-time students, people receiving disability benefits, and those considered "medically frail." That last category is defined broadly: if a serious health condition or disability significantly limits your ability to work, you likely fall under it.

SNAP: what changed

- Work requirements expanded. The rules now reach more people, including adults ages 55 to 64 without dependents, veterans, former foster youth, people experiencing homelessness, and parents whose youngest child is 14 or older. Most now have to show 80 hours a month of work, volunteering, or training, or they're limited to three months of benefits in a three-year window.

- The utility-bill change. How your heating and cooling costs get counted has shifted. Households without an elderly or disabled member may now need to submit actual utility bills instead of using a standard allowance. Federal estimates suggest hundreds of thousands of households, many with kids, could see roughly $100 less per month because of this alone.

- Timing. These changes have been rolling out state by state through 2026. Some benefit amounts and eligibility shifts apply at your next recertification, so the safest move is to recertify under current rules if you're due, and start keeping records now.

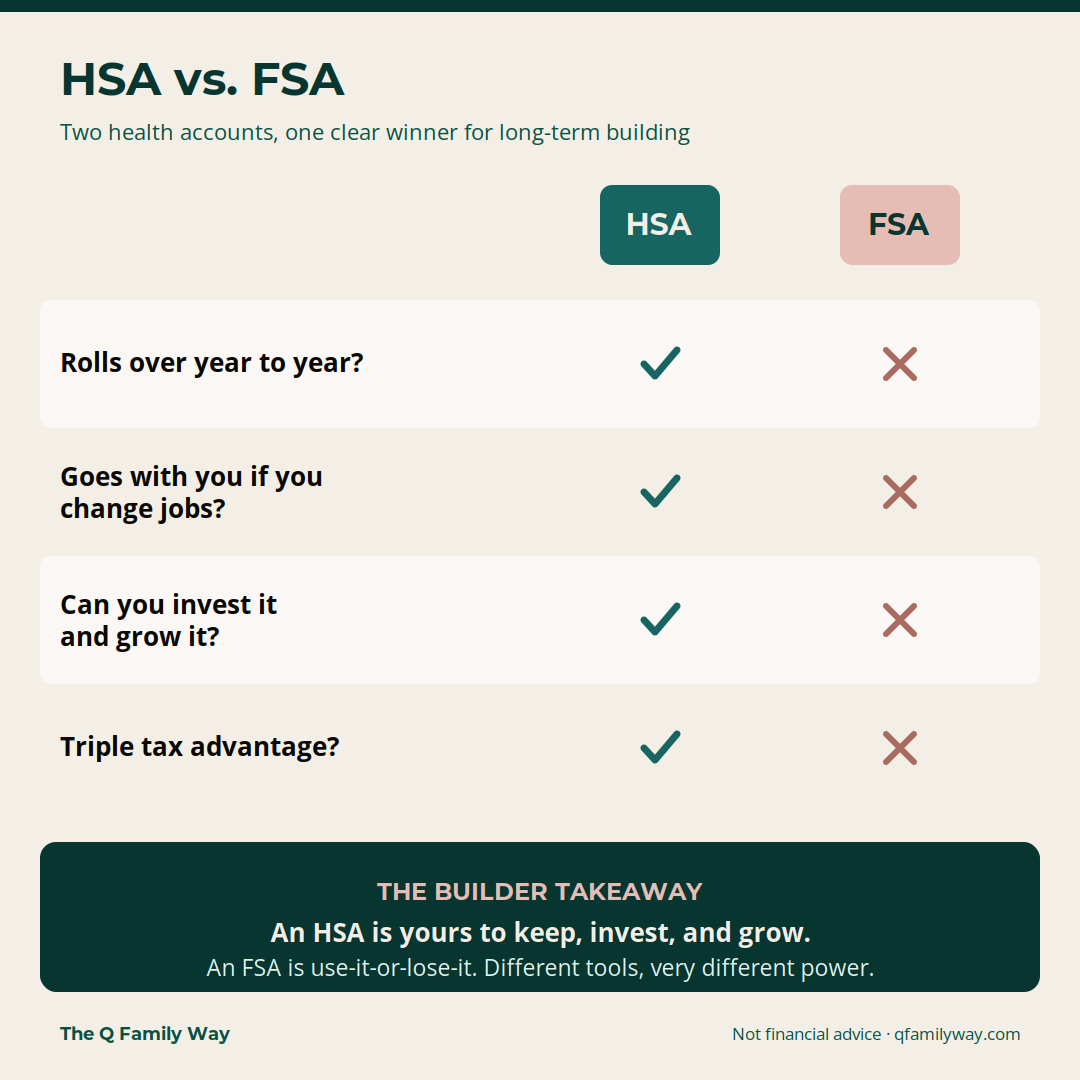

Clock Two: A Powerful Tool Just Got Easier to Use

Now the door that opened. If your family is on, or shopping for, a Marketplace health plan, this one is for you, and almost nobody is talking about it.

Starting in 2026, Bronze and Catastrophic ACA Marketplace plans now count as HSA-eligible. That's a big deal. For years, a Health Savings Account was mostly locked to people with specific high-deductible plans. Now millions more families, including a lot of self-employed and gig-working Builders on Bronze plans, can open one for the first time.

Why an HSA is worth your attention

An HSA is the only account that gives you a triple tax advantage: money goes in tax-free, grows tax-free, and comes out tax-free when you use it for qualified medical costs. Not a Roth. Not a 401(k). An HSA is the only one that does all three.

- 2026 contribution limits (per the IRS): up to $4,400 for individual coverage and $8,750 for family coverage, plus an extra $1,000 if you're 55 or older.

- It's yours, forever. Unlike an FSA, there's no "use it or lose it." The balance rolls over every year and goes with you if you change jobs.

- You can invest it. Most providers let you invest the balance in index funds once you're above a small cash minimum (often around $1,000). That's the piece most people miss.

The move I keep getting asked about

Here's the strategy behind the question I get most: if you can swing it, don't spend the HSA on today's medical bills. Pay small stuff out of pocket, invest the HSA, and let it grow. Save every medical receipt. There's no deadline to reimburse yourself, so a bill you pay out of pocket today can be paid back from your (much larger) HSA years from now, tax-free. After age 65, you can pull the money out for anything, taxed like a regular retirement account, which quietly turns your HSA into a bonus retirement fund.

Is that realistic for every family? No. If you need the money for care now, use it for care now, that's exactly what it's for, no guilt. But if you've got even a little breathing room, this is one of the most powerful, most overlooked wealth-building tools available, and it just opened up to a lot more of us.

The Bottom Line

Two clocks are running. One is asking you to prove you still qualify for support you've earned and rely on. The other is quietly handing you a tool to build a little more security for your family's future. Both reward the same thing: paying attention and moving a little early.

You are building a life for your family inside systems that weren't designed with you in mind. Reading this far is already the Builder move. Now go do one thing on that checklist.

Want the fuller conversation on how all of this lands for families navigating disability and healthcare? Pull up to the QFW Parenting Podcast for our latest episode, Built Different, Together: Parenting With and Through Disability. And if you're not in The Mix yet, the July Monthly Mix drops soon with more of exactly this plus extra Builder hacks.

Together, we make anything happen. Let's go, Q Fam.

Sources & Resources

- KFF · Work Requirement Provisions in the 2025 Federal Budget Reconciliation Law · kff.org

- Center for Health Care Strategies · Summary of Federal Medicaid Work Requirements (June 2026 guidance) · chcs.org

- Congressional Budget Office · coverage and spending estimates for H.R.1 · cbo.gov

- USDA Food & Nutrition Administration · SNAP OBBBA Implementation · fna.usda.gov

- Center on Budget and Policy Priorities · SNAP changes analysis · cbpp.org

- IRS · Notice 2026-05 and Rev. Proc. 2025-19 (HSA eligibility and 2026 limits) · irs.gov

- For your specific situation: your state Medicaid and SNAP offices, and a licensed tax professional or financial advisor.

Written by

What's Next?

Thinking About Longevity Should Start Now. And It's About Way More Than Money.

Millennial parents are officially middle-aged. I know, I cringed when I heard that as well. But, in all honesty, the oldest among us hit 45 this year, and with that milestone has come a question that none of us really planned to be asking in our parenting years: What kind of life am I actually building toward? Not just financially, but physically, socially, geographically. The whole picture. And in a system that wasn't designed with all of our needs in mind - as women, as trans people, as neuro

Mothering Is a Practice. Not a Title.

I was at the grocery store during #TeacherAppreciationWeek, picking up a few things for my kid's teachers, when I exchanged a "Happy Mother's Day" with the cashier and the bagger. But before I did, I added something I've been saying for a while now: It's a day for all who are mothering. Both women (people of color, different ages, different stages of life) didn't just nod, they actively agreed. Emphatically. Like I had said something out loud that they had been carrying quietly for a long time

Thinking About Longevity Should Start Now. And It's About Way More Than Money.

Millennial parents are officially middle-aged. I know, I cringed when I heard that as well. But, in all honesty, the oldest among us hit 45 this year, and with that milestone has come a question that none of us really planned to be asking in our parenting years: What kind of life am I actually building toward? Not just financially, but physically, socially, geographically. The whole picture. And in a system that wasn't designed with all of our needs in mind - as women, as trans people, as neuro